Being able to process credit card payments safely and knowing how to avoid common scams will protect your auto shop business and your customers in the long run. But despite your best intentions and efforts to prevent fraud and minimize the risk associated with accepting cards, you might still end up with a customer disputing a transaction that occurred with your shop.

The dispute process can be confusing to navigate. Understanding how disputes occur, what your responsibilities are, and how you should handle a dispute can give you a better chance of winning the case and ultimately keeping the funds. Here's what you should know:

What is a dispute?

A dispute, also called a chargeback, is a consumer complaint related to a credit or debit card purchase processed at your auto shop business. After your shop has completed a service or delivered a product, the consumer can contact their bank or credit card issuer within 180 days (or the allotted time frame from the issuer) to request a refund. If this happens, your business must pay a provisional credit to the cardholder while the transaction completes the dispute process.

A consumer might lodge a dispute if: They see an unauthorized charge on their account, the merchandise was not delivered or the service was not completed, credit wasn’t processed, or the service or product was not as described.

A dispute can be the result of:

Merchant error — An unintentional misstep on the business’ end. Some common examples of merchant errors include failure to clarify a return or refund policy, not following up on a customer complaint, listing inaccurate product descriptions, or accidentally charging a card twice.

Fraud — A fraudulent actor has obtained the cardholder’s information and used their card to make purchases in the cardholder’s name without their knowledge.

Friendly fraud — When a cardholder makes a legitimate purchase in their own name but intends to dispute it later. This can also happen when a family member who has access to a card makes unauthorized charges and the cardholder disputes the charges simply because they don’t recognize the purchase.

Regardless of what caused the dispute, it can negatively impact your business. If your shop has a high rate of disputes (1% or more of total purchases), it can lead to fines, higher fees, or even account termination. And, once a transaction is disputed, it cannot be intercepted or stopped — it must complete the full dispute cycle.

What to Do in a Dispute

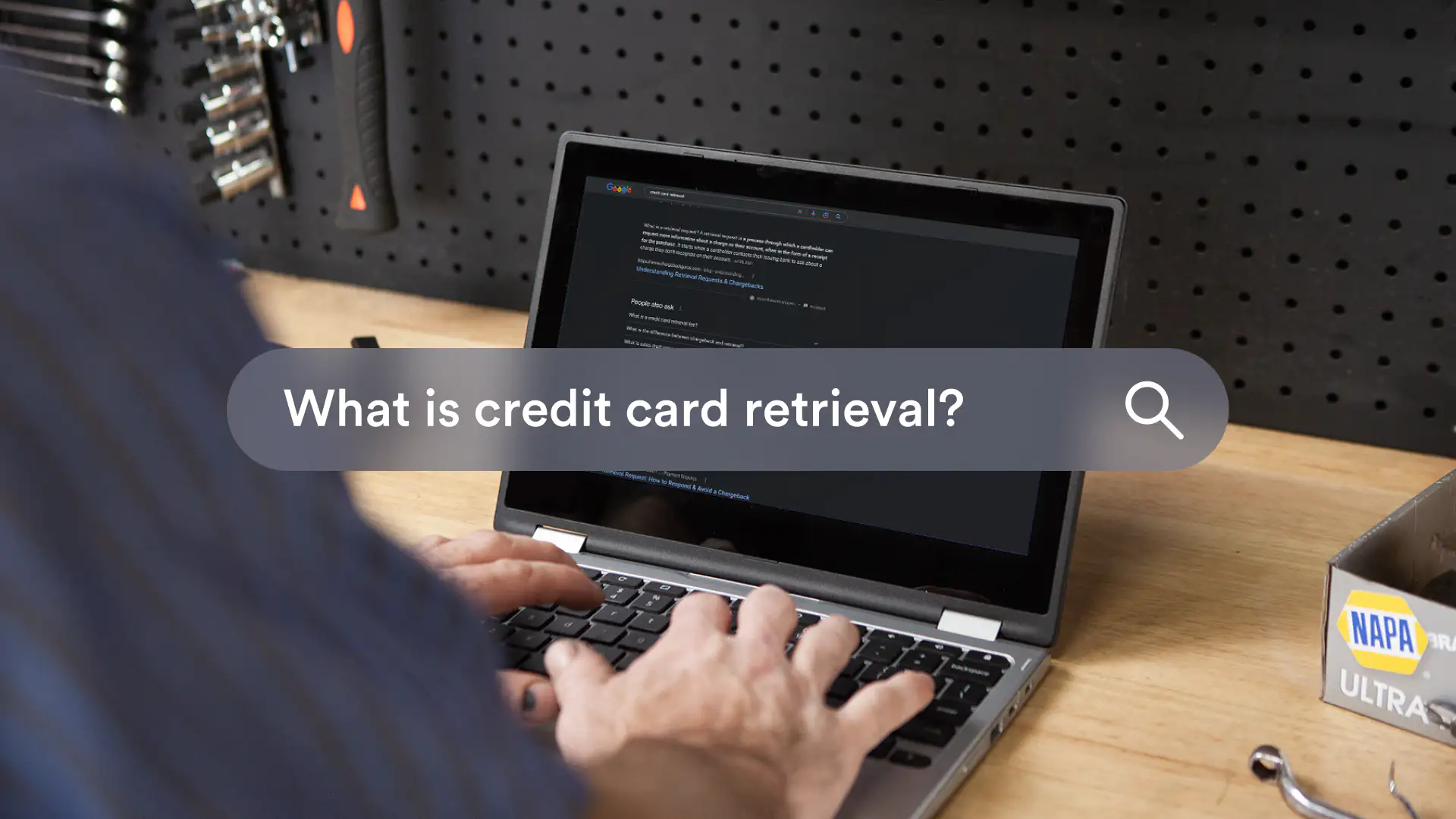

Some disputes begin as "retrievals".

A retrieval is not a dispute, but it could turn into one. It occurs when a cardholder contacts their issuing bank to inquire about a charge they do not recognize or have questions about. A retrieval is just an inquiry for more information on a card transaction — there is no financial impact to your business, but if the request isn’t handled properly, it can result in a dispute.

What to do:

Reach out to the customer during the retrieval period.

Supply all information and details related to the charge.

Try to resolve the situation directly with your customer.

Issue a proactive refund if you think this is the best course.

If you are in an official dispute:

You only have one opportunity to submit a dispute rebuttal, so it’s important to be intentional so that you do it right.

What to do:

Focus on delivering facts and evidence ON TIME. Note the rebuttal due date. You have to respond by this due date or you will automatically lose the dispute. This date is set by the cardholder's bank and will not be extended.

State only the facts of the purchase and communicate in a neutral, professional tone.

Gather compelling evidence to support your claim. Compelling evidence includes things like invoices, signatures, estimate approvals, shipping and delivery confirmation, logs of customer communication, and more — depending on the nature of the dispute.

Double check that your files are in accepted formats and don’t exceed the maximum size. Once you submit your response, it goes to the cardholder’s bank for review, and you can’t add any more documents or details.

Tip: Keeping a digital history of all services, invoices, customer approvals, and more can help you quickly prepare your evidence.

How is a dispute resolved?

The cardholder’s bank sets the deadline for when your compelling evidence is due. The bank will then review the case and issue a final verdict, which can take up to 45-60 days. Again, it’s crucial to meet the dispute deadline. If you don’t submit your evidence on time, the cardholder wins the dispute and gets to keep the funds. The cardholder’s bank will assume that you accept the dispute if you have not submitted evidence or provided no response by the deadline.

There are a few different ways that a dispute can ultimately be resolved:

You accept the dispute. This doesn’t mean that you’re admitting to any wrongdoing — it just means that you agree that the consumer deserves the refund.

You win the dispute. This means the bank or credit card company resolved the issue in your favor, and you’ll be returned the money and dispute fee.

You lose the dispute. This means the bank sides with the consumer, who keeps the money.

How can Shopmonkey help?

You can save yourself time and put yourself in the best position possible to win a dispute by having adequate documentation and evidence that can be quickly gathered. And when using Shopmonkey’s auto repair shop POS software, our team of risk experts will help you gather your evidence and compile the best rebuttal response to the cardholder's bank in the event of a disputed transaction. We can also help answer questions about suspicious transactions you encounter and provide guidance on how to proceed.

Need help implementing digital tracking of all service history with your customers and/or turning on integrated payments? Request a Demo